If you sold, traded, or otherwise disposed of cryptocurrency this year, the IRS requires you to report your capital gains and losses using Form 8949. This form is essential for ensuring that your cryptocurrency activity is properly documented and taxed.

We understand that reporting digital asset transactions can feel overwhelming, especially if you’ve used multiple wallets or exchanges. At CMP, we regularly guide clients through the crypto tax filing process and are aware of where mistakes commonly occur.

This guide provides a step-by-step breakdown of how to complete Form 8949 for cryptocurrency transactions. You’ll learn what information to gather, how to categorize transactions, how to calculate cryptocurrency gains & losses, how to avoid common mistakes, and how to submit the form properly. Whether you're filing yourself or working with a tax professional, by the end of this guide, you’ll know exactly what’s required to complete Form 8949 and report your crypto activity accurately.

What is Form 8949, and Why is it Important for Cryptocurrency Tax Reporting?

Form 8949 is a tax form used by the IRS to track capital asset transactions, including those involving cryptocurrency. If you’ve sold, traded, or otherwise disposed of digital assets during the year, you’ll likely need to report those activities on this form.

The main purpose of Form 8949 is to report capital gains and losses from the sale or exchange of property. In the case of cryptocurrency, each taxable transaction — whether it’s trading one coin for another, selling cryptocurrency for cash, or using it to purchase goods- must be documented.

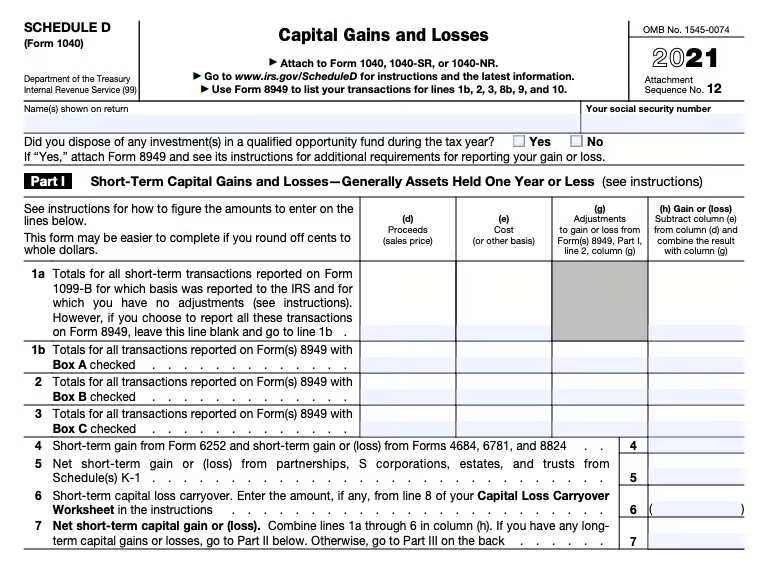

Form 8949 feeds directly into Schedule D (Form 1040), which summarizes your total capital gains and losses for the year. The IRS uses this information to determine how much you owe (or how much you can deduct) based on your crypto activity.

For cryptocurrency users, accurate reporting is essential. With increased IRS scrutiny of digital assets, failing to file properly or omitting transactions altogether can result in penalties, audits, or delayed tax returns. That’s why it’s critical to understand how Form 8949 works and how to fill it out correctly

Who Needs to Fill Out Form 8949 for Cryptocurrency?

If you’ve had cryptocurrency transactions that resulted in a gain, loss, or other taxable event, you need to report them on Form 8949. Here are some common situations where this form applies:

- Selling or trading cryptocurrency for a profit: If you’ve sold crypto and made a profit, you need to report this on Form 8949.

- Selling or trading cryptocurrency at a loss: Losses from cryptocurrency transactions must also be reported to offset gains or reduce taxable income.

- Using cryptocurrency to make a purchase: Even if you didn’t sell your cryptocurrency for cash, spending it on goods or services is considered a taxable event that must be reported.

There is one key exception: Self-directed crypto IRAs. If you're trading cryptocurrency within one of these tax-advantaged accounts, those transactions are not reported on Form 8949, as they're not subject to the same tax rules.

If any of these scenarios apply to you, you must complete Form 8949 for accurate tax reporting.

Step-by-Step Guide to Filing Out Form 8949 for Cryptocurrency

Filing Form 8949 can feel daunting, especially for cryptocurrency investors who have made numerous transactions across multiple exchanges. However, breaking it down step by step can make the process much more manageable. Follow these six steps to ensure you report your cryptocurrency disposals correctly and accurately.

Step 1: Take Account of All Cryptocurrency Disposals

Before you begin filling out Form 8949, it’s crucial to account for every cryptocurrency and NFT disposal you made during the tax year. Disposals are events like:

- Selling or trading cryptocurrency for another cryptocurrency or fiat currency.

- Using crypto to make a purchase (e.g., buying goods or services).

- Exchanging one crypto asset for another.

Regardless of which exchange or wallet you used, every disposition must be reported on Form 8949. Make sure to gather all relevant transaction records to avoid any missing data.

Step 2: Gather the Necessary Transaction Information

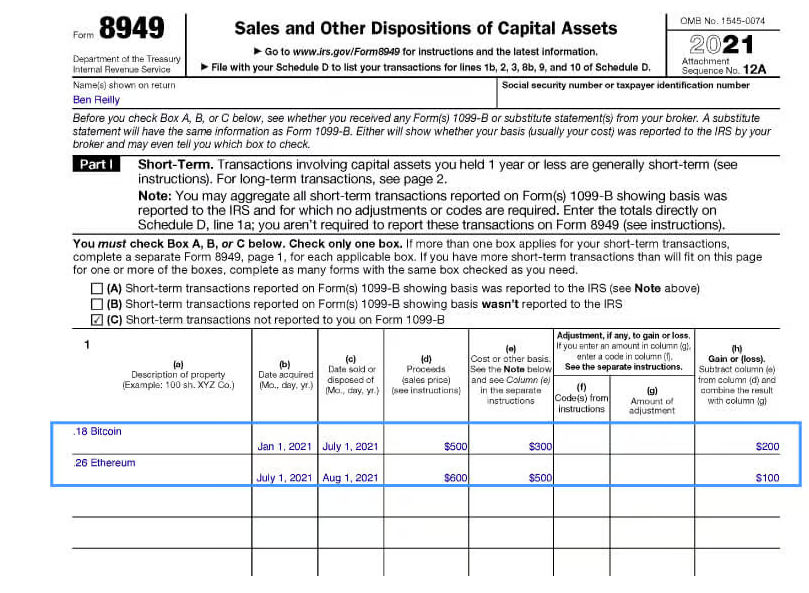

For each disposal event, you’ll need to collect the following information:

- Description of the property: For example, 1.5 BTC (Bitcoin).

- Date of acquisition: The date you originally purchased or acquired the crypto.

- Date of sale or disposal: The date you sold, traded, or used the cryptocurrency.

- Proceeds: The amount you received from the disposal.

- Cost basis: The amount you originally paid to acquire the cryptocurrency.

- Gain or loss: The difference between the proceeds and the cost basis.

If you haven't kept detailed records of your cryptocurrency transactions, it may be time to use cryptocurrency tax software, such as CoinLedger, to generate an accurate tax report. This software can help streamline the process and ensure you don’t miss any crucial data.

Step 3: Categorize Transactions as Short-Term or Long-Term

Form 8949 is divided into two sections:

- Short-term transactions: These are assets held for 1 year or less before disposal.

- Long-term transactions: These are assets held for more than 1 year.

Why does this matter?

- Short-term capital gains are taxed at ordinary income rates, which may be higher than those for long-term capital gains.

- Long-term capital gains are generally taxed at more favorable rates.

You’ll ensure you pay the appropriate tax rate by correctly categorizing your disposals.

Step 4: Select the Correct Reporting Option

You’ll need to select the correct checkbox for each transaction in both the short-term and long-term sections. The three options are:

- Transactions reported on Form 1099-B showing basis were reported to the IRS.

- Transactions reported on Form 1099-B showing basis were not reported to the IRS.

- Transactions not reported to you on Form 1099-B.

Most cryptocurrency exchanges do not provide a Form 1099-B, so you’ll likely need to select option 3. If you did receive a 1099-B from an exchange, choose either option 1 or option 2, depending on whether the basis was reported to the IRS.

Step 5: Report Each Disposal on Form 8949

Once you’ve categorized and selected the correct options, begin filling out Form 8949 with your disposal details. For each transaction, you’ll report:

- Date acquired: The date you first acquired the crypto.

- Date sold/disposed of: The date of the sale, trade, or use.

- Proceeds: The amount you received.

- Cost basis: The original amount you paid for the asset.

- Gain or loss: The difference between your proceeds and cost basis.

If you’ve disposed of collectible NFTs, you may need to report these separately on a different Form 8949 due to their different tax treatment.

Step 6: Transfer Your Totals to Schedule D

Once you’ve completed Form 8949, you’ll transfer the total short-term and long-term capital gains/losses to Schedule D, which summarizes your overall capital gains and losses for the year.

Schedule D helps calculate your total net gain or loss, which is then included in your overall tax return.

If you have any capital losses carried forward from previous years, don’t forget to include them in Schedule D to offset your current year’s gains, potentially. Following these steps will ensure that your Form 8949 is filled out correctly, minimizing the risk of errors and penalties.

Accurate reporting of cryptocurrency disposals is critical, so take your time and gather all necessary data. If the process seems overwhelming, consider consulting a tax professional or using crypto tax software to make your tax filing experience smoother.

How to Calculate Your Crypto Tax

Calculating your crypto tax might seem overwhelming, but once you understand what’s taxable, how gains are categorized, and how tax rates apply, it becomes much easier to manage.

Taxable Events in Crypto

You trigger a taxable event when you dispose of cryptocurrency. This includes:

- Selling crypto for fiat (like USD)

- Trading one crypto for another

- Using crypto to buy goods or services

- Receiving crypto as payment or from mining/staking

- Gifting crypto (over certain value thresholds)

If you’re simply holding your crypto, no tax is due yet—but as soon as you dispose of it, you're looking at a potential gain or loss that needs to be reported. And if you’re involved in activities like mining, you’ll also need to consider crypto mining tax implications.

Realized vs. Unrealized Gains

- Realized gains happen when you sell or trade your crypto—this is when taxes apply.

- Unrealized gains are changes in value while you're still holding the asset. These gains aren’t taxed until they’re realized.

Tax Rates for Crypto Gains

Because the IRS treats cryptocurrency as property, your gains fall under capital gains tax rules:

- Short-Term Capital Gains: For crypto held for one year or less, it is taxed at your regular income tax rate (10%–37%, depending on income).

- Long-Term Capital Gains: For crypto held over one year, taxed at 0%, 15%, or 20%, depending on your income bracket.

The Impact of Your Tax Bracket

Your total income determines how much you pay capital gains tax. Short-term gains are more costly since they’re taxed like regular income, while long-term gains benefit from lower rates.

Example: Calculating Crypto Tax

Let’s say Emma bought 0.5 BTC for $10,000 in January 2023 and sold it for $18,000 in March 2024.

- Holding Period: Over 12 months → qualifies as long-term capital gain

- Gain: $18,000 – $10,000 = $8,000

If Emma falls into the 15% long-term capital gains tax bracket, she would owe:

$8,000 × 15% = $1,200 in taxes on that sale.

Now let’s imagine she sells another crypto asset she held for just 6 months, earning a $4,000 profit. That would be taxed at her ordinary income rate (e.g., 24%), resulting in:

$4,000 × 24% = $960 in taxes for the short-term gain.

What Information to Provide on Form 8949 for Your Crypto Gains and Losses

When reporting your cryptocurrency transactions on Form 8949, accuracy matters. Each line of the form represents a single disposal event—whether you sold, traded, or used cryptocurrency in any way that counts as a taxable event. To complete the form properly, you’ll need to gather the following details for each transaction:

- Description of the asset – For example, “1.2 BTC” or “3.5 ETH.”

- Date acquired – The date you originally obtained the crypto.

- Date sold or disposed of – The date the transaction occurred (sale, trade, or use).

- Proceeds (in USD) – The fair market value of what you received at the time of disposal.

- Cost basis (in USD) – What you paid to acquire the asset, including any fees.

- Gain or loss – The result of subtracting your cost basis from the proceeds.

- Fees or commissions – Any transaction costs that affect the gain/loss calculation.

How to Submit Form 8949

Once you’ve finished filling out Form 8949 with your crypto transactions, you’ll need to submit it as part of your federal tax return. If you’re filing online, most tax software will let you upload or import the form directly and ensure the totals flow into Schedule D.

If you’re mailing a paper return, print Form 8949 and attach it behind your main Form 1040 after Schedule D. Be sure to keep any transaction records, such as CSV files from exchanges or wallet statements, in case the IRS requests them.

The standard tax deadline is April 15 for individuals, though businesses may have different due dates. If you need extra time to file, you can request an extension—but keep in mind that this doesn’t extend the time to pay any taxes owed.

Common Mistakes to Avoid When Filing Form 8949

When completing Form 8949 for cryptocurrency transactions, it’s essential to be as thorough and accurate as possible. Small mistakes can lead to inaccurate tax filings, penalties, or missed deductions. To help ensure you avoid costly errors, here are some common mistakes that many taxpayers make when reporting their crypto activities.

- Not reporting all transactions

- Incorrectly categorizing short-term vs. long-term holdings

- Overlooking transaction fees

- Missing out on cryptocurrency losses

- Poor record-keeping

Frequently Asked Questions About Filing Form 8949 for Cryptocurrency

As you work through completing Form 8949 for your cryptocurrency transactions, you may have some questions about the process. Many crypto investors face similar challenges when filing their taxes, so uncertainties are common. To clarify things, we've compiled answers to some of the most frequently asked questions regarding Form 8949 for cryptocurrency reporting.

Can I Use Tax Software to Complete Form 8949?

Yes, using tax software can make the process of completing Form 8949 much easier. Many tax tools allow you to automatically import your cryptocurrency transaction data, categorize your transactions, and generate the necessary reports. Popular options for crypto tax reporting include CoinTracker, TaxBit, and CoinLedger. These platforms can help streamline the process and minimize the risk of errors.

What is the Deadline for Filing Form 8949?

The IRS filing deadlines for individuals and businesses are typically the same as those for your regular tax return. For most taxpayers, the deadline for filing Form 8949 is April 15th. However, the deadline may be extended if the 15th falls on a weekend or holiday. Businesses may have different filing deadlines based on their fiscal year. It’s essential to stay updated on any changes to the tax calendar.

How Do I Report Crypto Losses on Form 8949?

Crypto losses are reported in the same way as gains on Form 8949. To claim a loss, list the transaction details, including the amount of loss incurred, and ensure you categorize the transaction correctly (short-term or long-term). If your losses exceed your gains, you may be eligible for a tax deduction and can carry the losses forward to offset future gains.

What if You Have Too Many Transactions on Form 8949?

Using crypto tax software is a good solution if you have numerous transactions, as it can efficiently handle bulk transactions. Alternatively, if you’re manually filing, you can attach additional sheets to Form 8949. Ensure that each transaction is clearly detailed and organized according to the provided instructions.

Do You Need a 1099 Form to File Form 8949?

You are not required to have a 1099 form to file Form 8949. However, receiving a 1099-B from an exchange can help simplify reporting by listing some of the necessary transaction details. If you don’t receive a 1099 form, you can still file Form 8949 by manually entering the required information from your transaction records.

Final Thoughts on Filing Form 8949 for Cryptocurrency

Filing Form 8949 for your cryptocurrency transactions doesn’t have to be overwhelming. By following the steps and ensuring all necessary details are reported accurately, you can simplify the process and avoid penalties.

If you’re unsure about handling multiple transactions or need extra help, consider using tax software or consulting a professional.

Need further assistance with your cryptocurrency tax filing? The CMP team is here to provide expert support and ensure you’re on the right track. Whether it's Form 8949 or other tax-related matters, contact us today for personalized guidance and strategies tailored to your unique needs.

Take control of your crypto taxes, and let CMP help you navigate the complexities with confidence!