When it comes time to file your income taxes, you want to be sure you take all the tax benefits available. Unfortunately, many eligible taxpayers miss out on tax deductions and credits because they are unaware they qualify. If you're saving for retirement, you may be eligible for the Saver's Tax Credit, also known as the Retirement Savings Contributions Credit.

At CMP, a Utah CPA firm, we work with taxpayers daily to ensure they don't pay more than necessary to the Internal Revenue Service (IRS) and state taxing agencies. Are you eligible for the saver's credit? Keep reading to learn what it is, how it works, and how much money you can save if you qualify.

What is the Saver's Tax Credit? Is the Saver's Tax Credit Refundable?

The Saver's Tax Credit is a non-refundable tax credit designed to encourage people to save for retirement. If you make contributions to an IRA, a Roth IRA, or an employer-sponsored retirement account during the tax year, you may be eligible to take a significant credit when you file your tax return.

The Saver's Tax Credit may also be available to people who contribute to an Achieving a Better Life Experience (ABLE) account on behalf of a disabled person. The credit percentage varies based on your adjusted gross income, with the minimum being 10% and the maximum being 50%. We will talk more about the credit rates later in this post.

How Does Saver's Tax Credit Work?

The Saver’s Tax Credit is simple in its structure. If you have a qualified retirement account, then you may qualify for the credit. The Saver's Tax Credit is calculated by multiplying the percentage you are eligible for, based on your adjusted gross income, by the total amount you contributed to retirement accounts during the tax year.

We mentioned above that this is a non-refundable tax credit. This means that the credit may not be used to increase your tax refund if you are due one or to create a tax refund if you wouldn't already have received one. It may be used to decrease tax liability, but it will not put money in your pocket.

Who Qualifies for the Saver's Credit?

The qualifications for the Saver's Tax Credit are relatively simple. According to the IRS website, people who qualify for this credit must have contributed money to a qualified retirement plan and meet the following three requirements.

- Age 18 or older

- Not a student

- Not claimed as a dependent on another person's tax return

For qualification, the IRS defines a student as someone who was either enrolled as a full-time student for at least five months of the tax year or took a full-time, on-farm training course given by a school or a state, county, or county local government agency. A school may be a traditional college or university or a mechanical, technical, or trade school.

There are income requirements as well. For 2021, your adjusted gross income may not exceed the following limits:

- $66,000 if married and filing jointly

- $49,500 if filing as head of household

- $33,000 for all other filers

If you meet the above requirements, you may be eligible to take the Saver's Tax Credit on your tax return.

Retirement Plans That Qualify for the Saver's Credit

One of the key requirements for taking the Saver's Tax Credit is contributing to a qualified retirement plan. Retirement savings contributions include the following:

- a traditional or Roth IRA

- Elective salary deferral contributions to an employer-sponsored account, including 401(k), 403(b), governmental 457(b), SARSEP, or SIMPLE plans.

- Voluntary after-tax employee contributions made to a qualified plan, including 403(b) plans or a federal Thrift savings plan.

- Contributions to a 501(c)(18)(D) plan.

- Contributions made to an ABLE account for which you are the designated beneficiary.

We should note that the inclusion of ABLE account contributions was new as of 2018. If you fall under the income thresholds we have listed above and made contributions to one or more qualified accounts, you probably qualify for the Saver's Tax Credit.

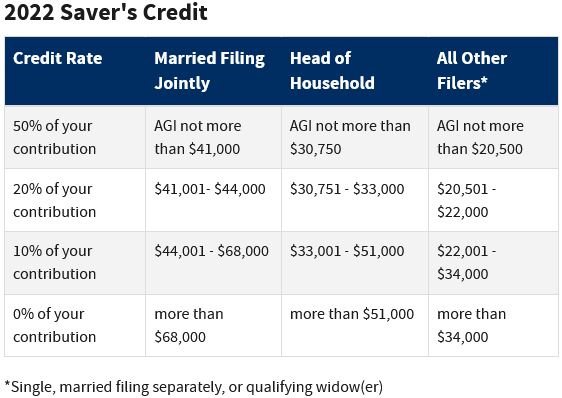

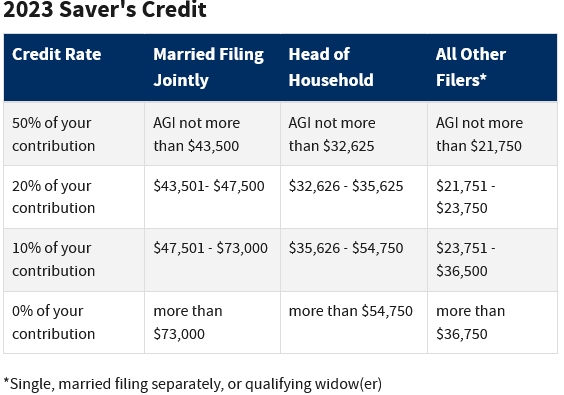

Saver's Credit Rates

The Saver's Credit has easy-to-understand rates that you can use to determine whether or not you qualify for a retirement savings contribution credit rate. Let's look at the rates for 2022 and 2023 from the IRS website.

The maximum percentage available to any taxpayer for qualified retirement savings contributions is 50%, and the lowest Saver's Tax Credit rate is 10%. If your income exceeds the maximum contribution amount listed above, you do not qualify for the saver's credit. There are also caps on the amount of the credit. The maximum credit is $1,000 for single filers and $2,000 for married and filing jointly.

How Much Could the Saver's Credit Cut from My Tax Bill?

Without knowing the specifics of your income, we can't tell you definitively how much the saver's credit could cut from your tax bill. However, we can give you a couple of examples to help you visualize how it works and what you might save.

Our first example involves Sally, a married executive assistant who earns a $40,000 salary. Her husband is currently unemployed. Sally contributed $1,000 to her employer-sponsored 401(k) plan and $1,000 to her individual IRA, for a total qualified contribution of $2,000. After making eligible deductions related to her contributions and student loan interest, Sally's AGI is $37,500. Since she and her husband are filing jointly, Sally is eligible for a 50% saver's tax credit totaling $1,000.

Our second example is Brendan, who is filing as head of household. He works in construction and earns $52,000 per year. After deducting his retirement and HSA contributions, his AGI is $48,000. If he contributed $3,000 to eligible retirement savings accounts, he would qualify for a 10% saver's credit of $300.

The quickest way to determine if you can qualify for the saver's credit is to calculate your AGI and compare it to the eligibility requirements. If you fall within the specified income thresholds, you may qualify for Retirement Savings Contributions Credit (saver's tax credit).

Does the Saver’s Credit Increase Your Refund?

One of the most common points of confusion with any tax credit or tax deduction has to do with refunds. You might think that if you qualify for a credit and it increases your tax refund (or results in a refund when you previously did not have one), that you would receive payment from the IRS in the amount of the credit.

The truth is that most tax credits are non-refundable, and that's the case with the saver's credit. Whether you filed as a head of household or you're married and filing jointly, your retirement contributions may qualify you for the saver's credit. So whether you filed as a head of household or are married and filing jointly, your retirement contributions may qualify you for the saver's credit. However, the credit amount will not be added to your tax refund if you're already getting one, nor will it earn you a refund if you previously would not have gotten one.

To understand what this means, let's look at an example. Let's say you contributed to an employer-sponsored retirement plan and would have owed $500 in taxes. However, you also made $2,000 of contributions to individual retirement accounts and would qualify for a saver's tax credit worth $1,000. What would happen is that your $1,000 credit would eliminate the amount you owe, evening you out with the IRS. The $500 of your credit that was not used to eliminate the amount you owe would zero out.

How to Claim the Saver’s Credit

Claiming the Saver's Tax Credit is easy. The IRS has created Form 8880 to help taxpayers determine their eligibility for the credit. You can find the form on the IRS website here.

If you are eligible to take the saver's credit, you will need to attach Form 8880 to your Form 1040, 1040A, or 1040NR. You may not claim the saver's credit with form 1040EZ, so you may want to work with a certified tax professional to file your taxes.

Conclusion

If you have made contributions to qualified retirement savings accounts, you may be eligible for the Saver's Tax Credit when you file your income tax return. The credit may be used to reduce the amount of income tax you owe.

Do you need help filing your taxes and determining if you qualify for the saver's credit? Contact us today to schedule your free consultation now!